How Organisations Fall Into PCI DSS Scope Without Realising It

TRENDING

PUBLISHED on

26

June

2026

In this blog, Alastair Stewart, Senior Consultant and QSA at URM, explains why organisations can still fall within Payment Card Industry Data Security Standard (PCI DSS) scope even when they do not directly store, process, or transmit cardholder data. He explores how factors such as system connectivity, third-party integrations, and user access can influence the security of payment environments. Through a practical example, the blog illustrates how incremental changes in technology and design can unintentionally expand scope. It concludes by emphasising the importance of proactively understanding and managing PCI DSS scope to avoid compliance gaps and reduce risk.

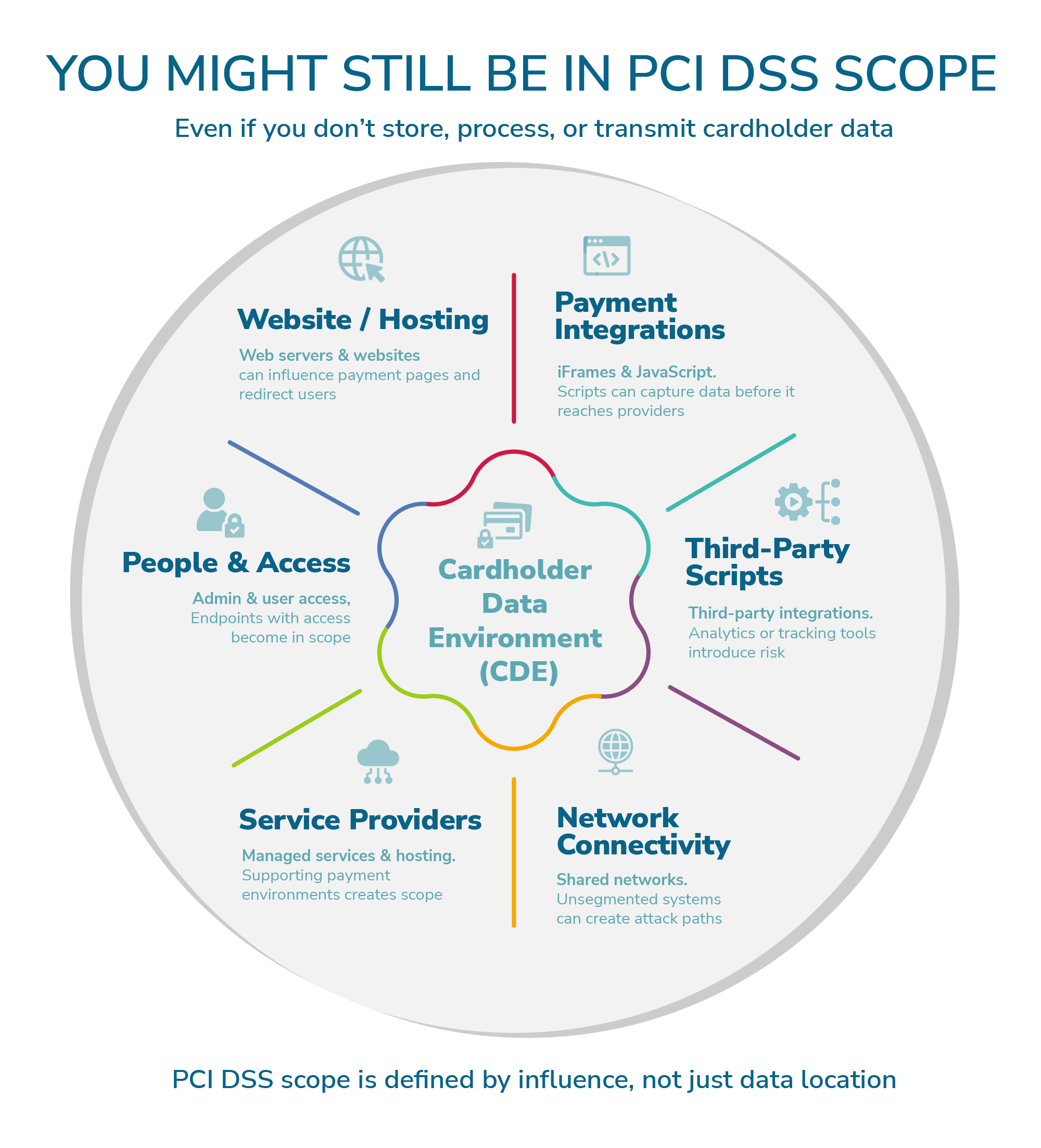

How can my organisation be in scope of PCI DSS when it doesn’t store, process, or transmit any cardholder data?

This is a question that any qualified security assessor (QSA) working in the field will have been asked countless times. Many organisations assume that not directly handling cardholder data automatically places them out of scope for PCI DSS, an assumption that is both common and risky. In practice, PCI DSS scope is determined not only by where card data resides, but by the ways that systems, people, and processes interact with environments that handle such data, even indirectly. As a result, organisations that never ‘touch’ card details can still fall within scope.

At its core, PCI DSS is concerned with protecting the entire cardholder data environment. This extends beyond obvious systems such as payment applications or databases. Any system that connects to, supports, or could influence the security of those systems may be considered in scope.

One of the most commonly overlooked scenarios involves outsourced payment processing. Most organisations in the present day outsource payment handling to third-party providers, assuming this removes their PCI obligations entirely. While outsourcing can certainly reduce scope, it does not eliminate responsibility. If your website redirects customers to a payment page hosted by a provider, your infrastructure may still influence the security of the transaction flow. A compromised web server could redirect users to a fraudulent payment page, meaning the organisation still plays a role in safeguarding cardholder data, even if it never sees it directly.

Similarly, integration methods matter. Techniques such as iFrame-based payment collection or JavaScript integrations can reduce exposure, but they do not automatically remove scope. If your systems host or deliver scripts that interact with payment forms, those systems become part of the trust chain. An attacker who compromises the hosting environment could inject malicious code to capture card data before it reaches the payment provider. In this situation, the organisation remains firmly within scope of PCI DSS because it controls part of the customer’s payment journey.

Another key factor is connectivity. PCI DSS considers systems connected to the cardholder data environment as potentially in scope, particularly if they can affect its security. For example, a shared corporate network that includes both general business systems and systems used to manage payment infrastructure creates a bridge. Even if a particular server does not process payments, its network connection could provide a pathway for attackers to move laterally. Without proper segmentation, the entire network may need to be treated as in scope.

Service providers also illustrate this point well. An organisation offering managed IT services, cloud hosting, or network administration may never handle card data directly. However, if its services support clients that do process cardholder data, it can be classified as a service provider under PCI DSS. This comes with its own set of requirements, including demonstrating compliance and ensuring that security controls protect client environments. The role played in supporting or managing infrastructure is enough to create scope.

People and processes can also expand PCI DSS scope in subtle ways. Administrative access is a common example. If staff within your organisation have remote access to systems that form part of a cardholder data environment, their endpoints and authentication mechanisms fall into scope. A compromised administrator account on a seemingly unrelated system could be used to gain access to payment infrastructure. In this way, human interaction becomes a link in the security chain, and therefore subject to PCI requirements.

It’s also important to remember that scope is dynamic rather than static. Business changes, such as introducing a new integration, migrating to cloud services, or altering network architecture, can unintentionally bring new systems into scope. Organisations that initially designed their environment to be out of scope may find themselves drawn back in over time if controls are not maintained or if new dependencies are introduced.

So, how does this happen in the real world? Let us consider a fictitious example to illustrate how organisations can unintentionally, and without realising, bring themselves into scope for PCI DSS.

Consider an online retailer, which has made a conscious decision to avoid handling cardholder data by implementing a hosted payment page provided by a well-known payment service provider. Customers browsing the retailer’s website are able to add items to their basket and, at checkout, be redirected to the provider’s secure payment page to enter their card details. Based on this design, the retailer assumes it is entirely out of PCI DSS scope.

However, over time, the organisation introduces changes to improve the customer experience. It adopts a JavaScript-based integration that allows the payment form to appear embedded within its own checkout page rather than redirecting customers away. The script responsible for rendering the payment form is hosted on the retailer’s web server. The marketing team also decides to deploy additional third-party scripts for analytics and user behaviour tracking, all loaded dynamically on the same checkout page.

During a routine security review, it is identified that the web server hosting these scripts has not been hardened to PCI DSS standards. It also shares infrastructure with other non-critical web applications. More importantly, no controls are now in place to monitor or restrict changes to the scripts being served to customers. This creates a clear risk: if an attacker compromises the web server or a third-party script, they could inject malicious code to capture card details as users enter them, despite those details ultimately being submitted to the payment provider.

At this point, the retailer’s environment is now deemed to be in scope for PCI DSS. The organisation is not storing or processing card data itself, but it controls a critical part of the payment page delivered to customers. Its systems can now directly affect the security of cardholder data in transit. As a result, the retailer needs to implement additional controls, including file integrity monitoring, stricter access management, network segmentation, and ongoing vulnerability management for the in-scope systems.

The lesson from this scenario is straightforward. Even well-intentioned design decisions aimed at reducing PCI scope can be undermined by incremental changes and dependencies. What begins as a clean separation between the organisation and cardholder data can evolve into a tightly coupled environment where security responsibilities return, often unnoticed.

In conclusion, not handling cardholder data directly does not guarantee exemption from PCI DSS. Scope is defined by influence, connectivity, and trust relationships, not just data storage. Organisations that underestimate this often discover their obligations only after a security review or incident. A proactive understanding of how systems interact with payment processes is therefore essential, both to maintain compliance and to reduce the risk of compromise.

URM provides structured, end-to-end support to help organisations achieve and maintain PCI DSS compliance in a practical and efficient way.

Establishing a clear understanding of your current position and obligations:

Guiding you through the steps required to achieve and sustain compliance and facilitating a smooth and successful PCI DSS assessment:

URM’s experienced QSAs ensure your approach is not only compliant, but also efficient, risk-focused, and aligned with your business operations.

A short, free, non‑commitment call can help you clarify scope, understand regulatory expectations, and align your approach across standards such as ISO 42001 and NIST AI RMF. Early guidance often saves time and avoids fragmented compliance efforts.

Whether you are at an early planning stage or preparing for audit and assurance activities, we offer a free introductory call to help you assess risks, responsibilities, and the most proportionate route forward.

You do not need a fully defined programme to start the conversation. We offer a free, no‑obligation call to help you understand SOC 2 requirements, assess your current position, and identify practical next steps.

URM’s blog explains the recent update to PCI DSS SAQ-A that has resulted in the removal of 2 new v4 requirements & the addition of new eligibility criteria.

URM’s blog explains how organisations can unintentionally and without realising fall into scope of the PCI DSS, despite not directly handling card data.

While it’s one of the areas that IT and security departments find challenging, documentation (and compliant evidence)....